SMM, June 13:

Metal Market:

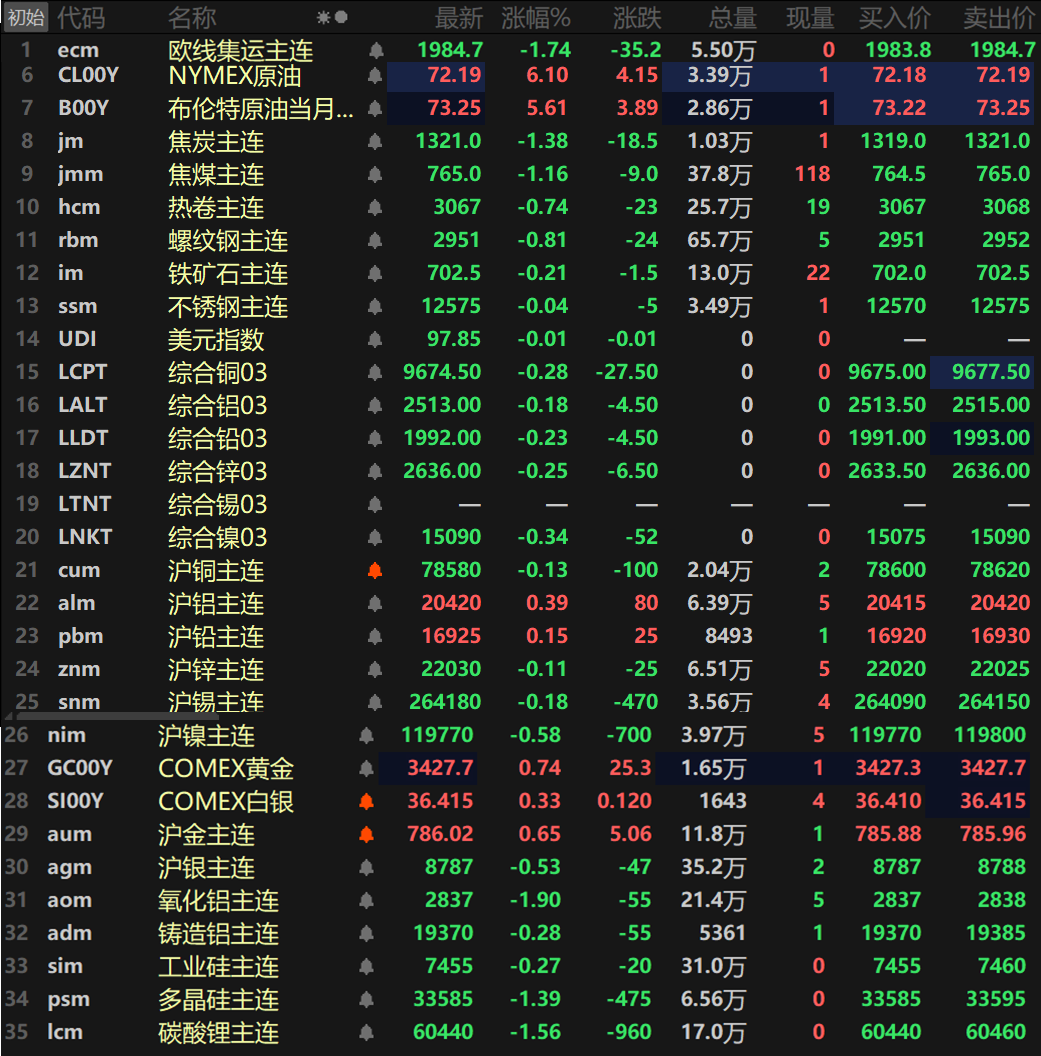

As of the overnight close, domestic market base metals generally declined, with only SHFE aluminum and SHFE lead rising together. SHFE aluminum increased by 0.39%, and SHFE lead rose by 0.15%. SHFE nickel led the declines with a 0.58% drop, while the declines in other metals fluctuated slightly. In the overseas market, base metals showed mixed performance, with LME copper, LME aluminum, and LME lead rising together, but the fluctuations in the percentage changes of these metals were relatively small. LME nickel recorded five consecutive days of declines, with the main alumina contract falling by 1.9% and the main aluminum casting contract dropping by 0.28%.

In the ferrous metals series, prices fell collectively. HRC declined by 0.74%, rebar fell by 0.81%, and iron ore dropped by 0.21%. In the coking coal and coke sector, coking coal fell by 1.16%, and coke declined by 1.38%.

In the overnight precious metals market, COMEX gold rose by 1.88%, recording two consecutive days of gains. After opening on the morning of June 13, it surged again, touching a new high since May 7 during the session, driven by escalating regional tensions and cooling US economic data fueling a new round of bets on a US Fed interest rate cut. COMEX silver rose by 0.41%. Domestically, SHFE gold increased by 0.65%, while SHFE silver fell by 0.53%.

As of 8:23 a.m. on June 13, the overnight market close on Friday

》Click to view SMM Futures Data Dashboard

Macro Front

Domestic:

[PBOC and SAFE: Further Strengthen Financial Support for Cross-Strait Integration and Development] The "Measures" include optimizing the financial ecosystem for the shared "living circle" across the Taiwan Strait, serving Taiwan compatriots and Taiwan-funded enterprises in building the first home for landing, supporting high-level opening-up pilot programs for cross-border trade in Fuzhou, Xiamen, and Quanzhou, and facilitating cross-border investment and financing under the capital account. The PBOC and SAFE will promote the detailed implementation of various policy measures outlined in the "Measures."

On the afternoon of June 12, the Ministry of Commerce held a regular press conference, where a reporter asked about the first meeting of the China-US economic and trade consultation mechanism. He Yadong, spokesperson for the Ministry of Commerce, stated that from June 9 to 10 local time, the China-US economic and trade teams held the first meeting of the China-US economic and trade consultation mechanism in London, UK. The two sides reached a consensus in principle on measures to implement the important consensus reached during the phone call between the two heads of state on June 5 and to consolidate the outcomes of the Geneva economic and trade talks, making new progress in addressing each other's economic and trade concerns. Regarding rare earths, as a responsible major country, China fully considers the reasonable needs and concerns of various countries in the private sector and reviews export license applications for rare earth-related items in accordance with laws and regulations. It has already approved a certain number of compliant applications in accordance with the law and will continue to strengthen the approval process for compliant applications.

US dollar:

As of overnight close, the US dollar index fell by 0.78%, hitting a low of 97.6 during the session, the lowest since March 2022. US inflation data for May came in below expectations, suggesting that the US Fed may resume interest rate cuts as soon as possible. Data showed that the month-on-month (MoM) increase in the US Producer Price Index (PPI) for May was lower than expected, suppressed by a decline in service prices such as airfares, which weighed on the US dollar. Wednesday's data also showed cooling inflation, with the US Consumer Price Index (CPI) rising less than expected.

The futures market tracking the US Fed's policy rate increased its bets on two consecutive interest rate cuts starting in September. Before the data release, the market was betting on an interest rate cut in September and another in December.

Other currencies:

The safe-haven Japanese yen and Swiss franc were boosted by escalating tensions in the Middle East.

The euro rose to its highest level against the US dollar in nearly four years. The US dollar fell to a two-month low against the Swiss franc and to about a one-week low against the yen.

In afternoon trading, the US dollar fell more than 1% against the Swiss franc to 0.8114 Swiss francs, after earlier hitting a low of 0.8104, the lowest since April 22. The US dollar fell 0.7% against the yen to 143.59 yen, after earlier touching a one-week low.

The euro against the US dollar once touched $1.1632, the highest since October 2021, and ended the New York session up 0.8% at $1.1576.

Data:

Today, the preliminary US University of Michigan Consumer Sentiment Index for June, the eurozone's seasonally adjusted trade balance for April, the eurozone's total reserve assets for May, the final annual rate of Germany's CPI for May, the monthly rate of Canada's manufacturing sales for April, and the monthly rate of Canada's manufacturing new orders for April will be released.

In addition, the US Fed released the "Quarterly Financial Accounts Report for the United States," and He Lifeng visited the UK from June 8 to 13 and held the first meeting of the China-US Economic and Trade Consultation Mechanism.

Crude oil:

As of overnight close, oil prices in both markets rose together, with US crude oil up 1.04% and Brent crude oil up 0.82%. This was due to traders choosing to take profits after the previous trading day's surge of over 4%. The reason for Wednesday's oil price increase was concerns about disruptions to Middle Eastern oil supplies.

The US decision to withdraw personnel from the Middle East led to both benchmark crude oils rising over 4% on Wednesday, reaching their highest levels since early April. StoneX Energy analyst Alex Hodes said that from multiple technical indicators, this surge pushed the market into overbought territory, so a short-term correction may be needed.